News

9M 2014 Results

27-10-2014

9M 2014 RESULTS

Adjusted EBITDA at constant currency (215 million euros) increases by 7.4% (although it slows down in to +2.1% in 3Q)

- Advertising in Spain shows weak signs of recovery during the year but it has changed since September to a positive trend. In Portugal, the advertising recovery is being consolidated.

- Solid growth in Latin America in local currency (in Santillana and Radio), despite a slowdown in the economic growth of some countries (mainly Brazil and Chile).

- Cost reduction and control of CAPEX continues across all business areas.

Focus on the execution of the Refinancing Plan

- 780 million Euro of debt cancelled to date and agreement for sale of Canal+ reached with Telefónica.

- High visibility of reaching the 1.5 bn debt amortization commitment.

Advertising in Spain shows an irregular trend during the year

- In Spain, adjusted advertising revenues of the Group have been irregular, decreasing by

-2.4 %. After three irregular quarters, September shows growth.

- In Radio local advertising revenue consolidates its growth trend (+4.4% cumulative growth), with positive growth in each of the preceding 9 months. National advertising revenue does not show a clear trend yet. Press slows its decline in the last three months.

- In Portugal, advertising revenues, in Media Capital grow by +14.1% (+14,8% in TVI and +9,7% in MC Radio).

Latin America activities show solid growth in local currency but negative FX impact

- Solid growth in local currency in Education (+9.9%) and Radio (+4.6%) excluding the impact of the change in consolidation perimeter. Third quarter (+24.3% and -8.6% respectively) was impacted by the economic slowdown in the area and by the Soccer World Cup.

- Negative impact from FX evolution that reaches 73.4 million Euros in 9M 2014 revenues, 22.6 million at EBITDA level (55.5 in revenues and 15.4 in EBITDA in 1H).

- 62.5% EBITDA of the Group from Latin America at constant currency.

The Group continues its transformation

- Adjusted digital advertising grows by 14.8%.

- In the press division, digital advertising represents 30% of advertising revenues (+32.1% in 3Q).

- An average unique browser to the Group’s web sites grows by 15% reaching more than 88 million.

- Digital education systems continue their development in Latin America, improving margins significantly (increase of 15 million contributions at EBITDA level).

OPEX and CAPEX control continues

- Fall in all operating expenses of 57.7 million euros (-6.1%).

- Adjusted personnel expenses fall by 28.1 million Euros (-8.9%): Spain (-13.5%) ;Portugal (-3.3%) and LatAm -3.9%.

- The entire collective agreements have been renewed and voluntary severance and de-indexation agreements have been reached in several areas.

- CAPEX review to channel resources to growth areas, mainly Santillana.

The Group continues with its focus on the execution of the refinancing plan

- The Group continues with its focus on the execution of the refinancing plan: €780 million debt cancellation by the repurchase of debt by back at 25% discount with funds coming from:

- €100 million capital increase at 0.53 euros per share.

- Sale of 13.68% stake in Mediaset Spain.

- Agreement for the sale of 56% stake of Canal + to Telefonica with an initial price of 750 million.

- The total net debt of the Group as of September 30th amounts to 2,599.72 million (2.500 million euros of gross debt at corporate level) comparing to 3,300.76 million Euros on December 2013.

Results by business division

Education

- In 9M 2014 all the campaigns from south Area have been closed showing mainly a good performance in local currency.

- Remains to be closed the Campaigns of Spain, Mexico and the institutional of Brazil, fundamentally.

- Spain: the educational Campaign, which carried out a delay as of June, is showing as of September a good behaviour, despite the difficulties on the implantation of the new education law and thanks to the commercial effort and cost control. Revenues grow by 3.2% and EBITDA by 5.4%. Despite still to be closed, it is expected to end with growth compared to 2013.

- Brazil: the institutional sale still to be registered. Considering that the volume of government purchases has been lower than expected and that prices have not fully been impacted by inflation, it is considered unlikely to maintain the same volume of revenues as previous year in spite of holding the same market share.

- Mexico: The campaign has developed its performance as expected and should not show significant changes for the year end.

- Digital education systems (UNO) continue their development in Latin America, significantly improving their profitability: EBITDA of 13.8 in 9M 2014 versus -1.3 EBITDA in 9M 2013.

- The adjusted revenue in local currency increased by +8.2% (Spain 3.1%, Brazil 6.5%, Mexico 4.3%, Argentina 41,8 %, Chile 16,5%). Exchange rate has a negative impact on revenues of 61.7 million in Santillana 9M 2014, 58.8 million in 1H 2014.

- Adjusted EBITDA grows by 14.1% in local currency (-0.6% in Euros), within FX impact of 20.3 million euros.

Radio

- Advertising in Spain falls by -2%, showing a worse performance in July and august, due to seasonal effects, such as Football World Cup that had a negative impact, mainly in the Radio business. A positive change in the trend is reflected in September, which is expected to be maintained towards the end of year.

- Advertising in Latam grows in local currency in all countries. Reported results are impacted by:

- FX has a negative impact in radio revenues of 10.9 million Euros (2.2 million in EBITDA).

- Change in consolidation of Mexico & Costa Rica, which is integrated through equity on the back of an international accounting law change, adopted by the EU and which impacts since January 2014.

- Excluding this impact, advertising revenues in Radio Latam would have grown by 5.3%, with a worse 3Q in Chile (impacted by the government change) and Colombia (we expect a recovery over de year).

- Effort in cost control continues (-4,8% in adjusted terms),mainly in staff costs (-8.4% over the period).

- Adjusted EBITDA in Radio reached 37 million Euros in 9M 2014 (+13.5 in respect 9M 2013 and 20.3% FX adjusted). In 9M 2014 adjusted EBITDA in Spain improve in 6.4 million Euros.

Press

- Advertising revenues fall by -3.8% (El País -8.1% y AS +14.8%).

- In adjusted terms, traditional advertising revenues fall by -15.2% which are partially compensated by the excellent performance of the Digital advertising revenues which grow by 19.3% and already represent 30% of the division’s advertising revenues and by revenues from new business (event management) which grow by 30%.

- We highlight the strength of AS where digital advertising revenues grow by 27.4% and already represent over 50% of the total.

- Circulation revenues fall by -16.7%.

- Strong growth in Other Revenues (16.2%), mainly promotions. In 9M 2014 revenues no deductions have been recorded. During 9M of 2013, 4.7 million euros worth of deductions were registered as revenues.

- Strong cost control in every item (-2.8% in adjusted terms and -9.5% in staff costs).

- Adjusted EBITDA in press reaches 5.3 million Euros (-58.3% compared to 9M 2013 or -33.4% adjusting for deductions recorded in 2013 and not registered in 2014).

Media Capital

- Advertising Revenues increase by +14.1% in 9M 2014 (1Q, +5.3%; 2Q, +26.4%; 3Q, 8.7%). Very good performance both on TV (+14.8% in 3Q 2014) as well as on radio (+9.7%). It is worth noticing that advertising recovery in Portugal started in second half of 2013).

- Decline in other income in 9M 2014 (-19.3%), mainly due to drop in value added call services.

- Adjusted EBITDA reaches 25.4 million Euros and grows by 5.6 % on the back of the stability of Revenues and a strong effort to control the costs.

Sale of Canal+

On June 2014 the contract to sell 56% stake of Canal+ with Telefonica was formalized at initial amount of 750 million euros:

- The price is subject to customary adjustments in such operations until the closing of the transaction plus an specific adjustment depending on the resolution of the arbitrage wit Mediapro concerning the costs of the 2012-2015 football seasons.

- The operation is already approved by the representative panel of the financing banks and is only subjected to the authorization of the competition authorities.

- The administrative inquiry of the operation has been transferred by the EU authorities to Spanish supervisor body, the CNMC (National Commission for Market and Competition). This case is currently being processed by the commission.

- The signing of the agreement generates an accounting loss in the consolidated accounts of Prisa of 2,064 million euros and 750 million in the individual accounts, This loss in the individual accounts generates an asset imbalance, that was offset by an automatic conversion of a portion of tranche 3 of the corporate level debt, into equity loans for a sufficient amount to compensate for this asset imbalance.

- This conversion was provided for in the refinancing agreement signed by the company in December 2013.

- The amount of debt from Tranche 3 that was converted into equity loans (PPL's according to the contractual definitions), was 507 million euros and took place on September 15th 2014.

- The results of this transaction are presented in the consolidated income statement under "Result from discontinued operations" and the assets and liabilities as "Non-current assets held for sale" and "Liabilities associated with non-current assets held for sale".

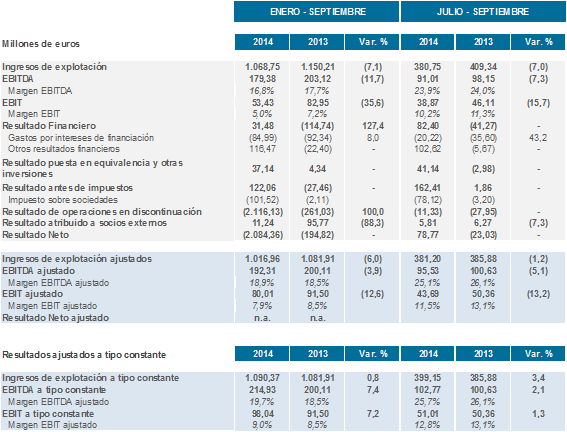

Consolidated P&L

The comparison of the results of the first half of 2014 and 2013 is affected by extraordinary items recorded under both revenues, expenses, amortizations & provisions. To conduct a homogeneous comparison, we are presenting a profit and loss account adjusting these extraordinary items:

During the first 9M months of the year, excluding extraordinary items and exchange rate:

- Operating revenue grow by 0.8%

- Adjusted EBITDA grow by 7.4%.

- The improvement in margins continues.

It may interest you